Part 5 - USE CREDIT CARDS FOR PAYMENT ACCOUNTS

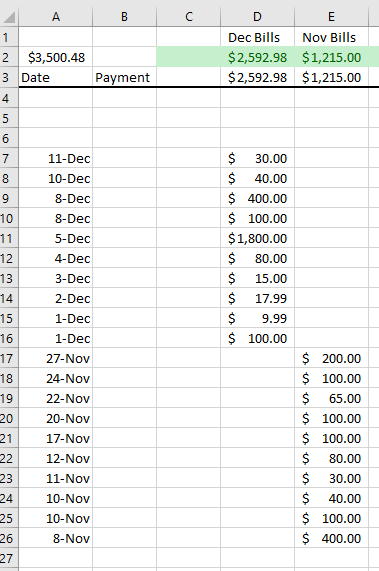

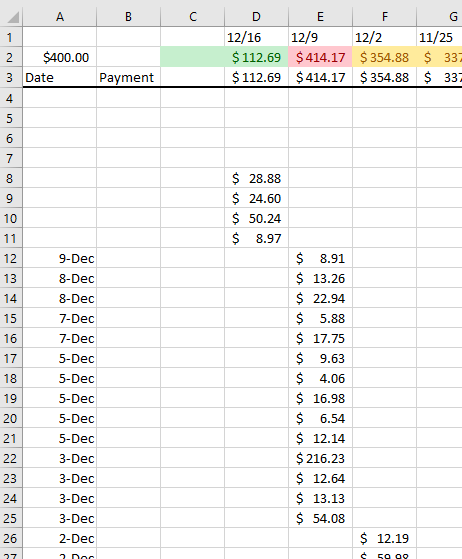

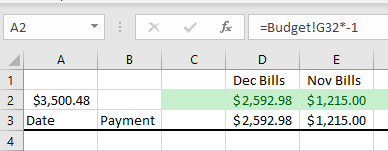

We are ready to start Phase 2 of our planning. This process will incorporate a few additional components and give us better tracking and control of our spend. So, to level set where we are I have filled out our spending for the past couple weeks. On my Payment Acct 1, I added a column for December and copied over the formulas for cell D2 and D3. On Payment Acct 2, I created new columns for each week and adding the sample spending amounts for each of those days. They now look like this:

One specific item to note is that on the week of 12/9, I went over budget. In this case it was by $14 which I can see easily offsets by the week before when I was $46 under budge, so I am not too concerned. If I didn’t have that extra savings, I know that for this week I need to try to make that up by saving a little more this week.

On my monthly bills, they are still all expected and I am in the green. We haven’t had a full month of tracking, but we would expect these expenses to be consistent and not change very much.

Our next step is to rename our Payment Accounts to Credit Card 1 and Credit Card 2.

I use credit cards for everything I can. There are a couple reasons. First, credit cards are spending someone else’s money, this means if I have a dispute on a charge, it is not out of my bank account yet. I can work with the credit card company to resolve the issue. Second, I can leverage the extra credit in the event I have an expense that is unexpected. Third, I get benefits from the credit cards I use. We will cover more later in this series. Last, and the most important part, I use the credit cards as a transactional medium. They are paid off every month and never carry a balance; therefore, I never pay interest on those cards.

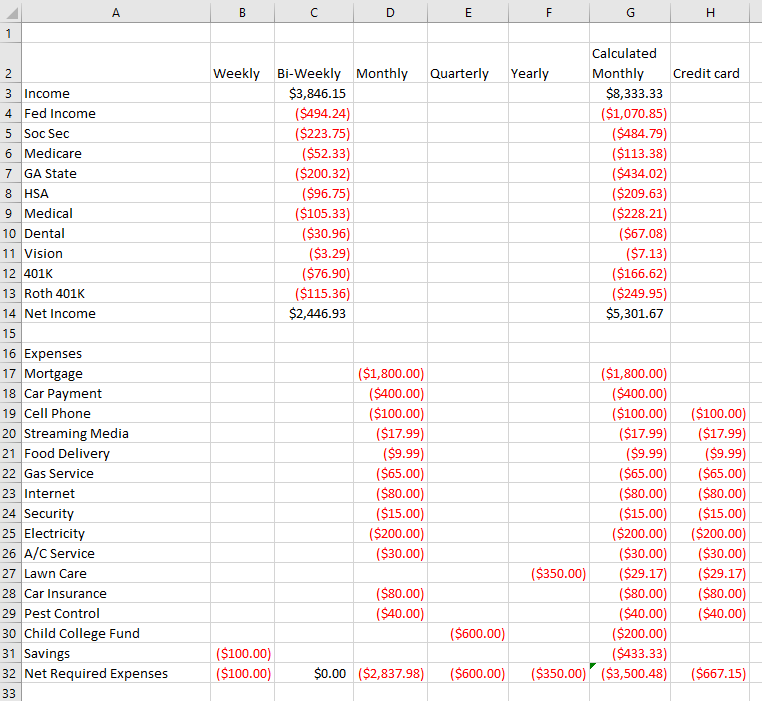

Now that we are planning to use credit cards for our weekly discretionary spending and our monthly expenses, we need to make a few adjustments to our budget.

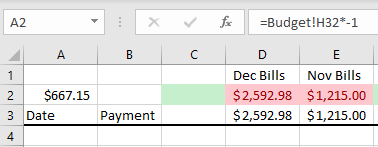

On our budget, I added a new column (H). In this column I labeled expenses from column G that I plan to use via a credit card. My mortgage, car payment, child college fund, and savings are not expenses I can pay with a credit card, so they are now empty. I now have a target of $667.15 for that credit card payment.

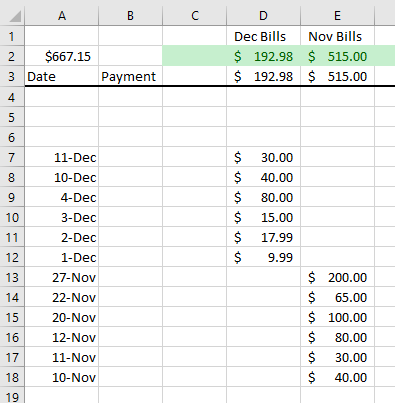

I will now go update the formular on Credit Card cell A2 to reflect the new column of target expense.

Unfortunately, we now are showing red for our spending. To correct this, we now need to remove the payments from our history, knowing that now these will be paid via this credit card in the future and those other expenses will be covered directly from our bank account.

We have now converted our tracking to use credit cards as our normal means of payment. Next week we will add tracking for paying off those credit cards to ensure we are always ahead of the payment schedule, we never pay interest, and we don’t fall behind with any of our expenses.

Thank you

Brian