Part 2 - BUILD YOUR INITIAL BASIC BUDGET

Part 2 of this series is extending part 1, but adding in a few more parameters to your financial picture, then tweaking them for an initial target. Remember there are no right or wrong answers right now. This is all about getting a starting point and building a picture where you can focus on 1 piece at a time.

Let’s bring up where we ended in Part 1. We are going to add a few more lines to this worksheet before we move on to the next part.

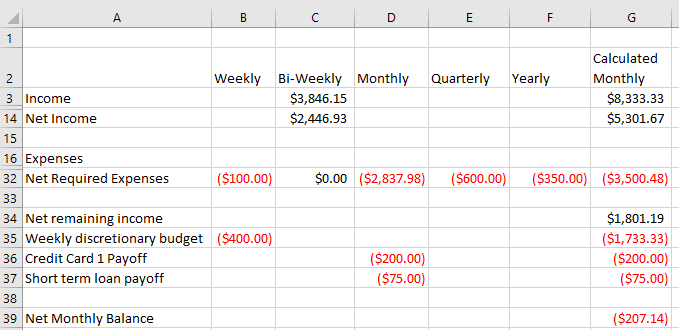

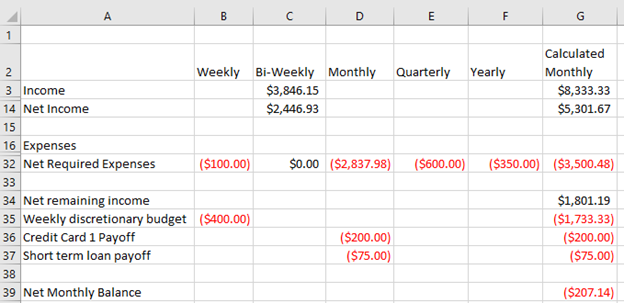

Below our net remaining income, we are going to add an entry for what we guess we spend weekly for our discretionary budget. This discretionary budget is for food, gas, household items, gifts, etc. Everything that is not generally the same every month and you have more control over. This step is important to include as we will use it later. I also added 2 other items that are not permanent expenses, but in the example are important to the person’s plan. I included a credit card that I may be working to pay off, and a short-term loan, maybe I purchased a new piece of furniture for 0% at 24 months. These are important to include but may not be there forever.

Now we have a great picture of where we stand at the current time. There is a red flag here. The net monthly balance is red, this means it is negative.

This is one of the most important components to understand when going through this process and it can be a very small difference on paper that makes the most important difference to you and a stress-free finance picture. In this case $207.14 every month goes out the door. For a year that is almost $2,500 and for 5 years it is $12,428.4.

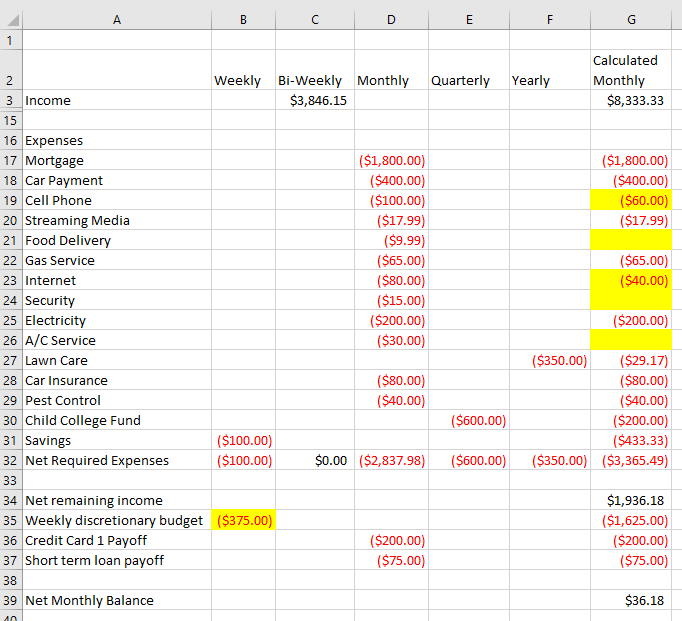

In this example, I picked a few items to tweak to change my net balance to a positive one. In this case I found a cell phone plan for $40 / month less, I cut my food delivery bill, I moved to a cheaper Internet plan, cut my security system, and cut my monthly A/C service retainer. I also cut $25 / week out of discretionary expenses. These minor changes could put me positive for the month. The net for 1 year is $434.16 or for 5 years $2,170.80. Can you imagine the difference in your stress level over time just by making your bank account grow a little every month instead of decrease, all while meeting all of your financial requirements?

These tweaks can be made now or can wait until we get to another phase. The choice is up to you. If you are tight on savings, it may be more important to make some of these changes now. If you have a little room to continue to let the process work for you, then maybe you leave these items alone for now until you have a full understanding of your habits.

In our example we are going to remove these tweaks and go back to our negative net monthly balance.

Next part we will start tracking our spending on a weekly basis. That will help us see just our discretionary spending on a week-by-week basis.

Thank you,

Brian